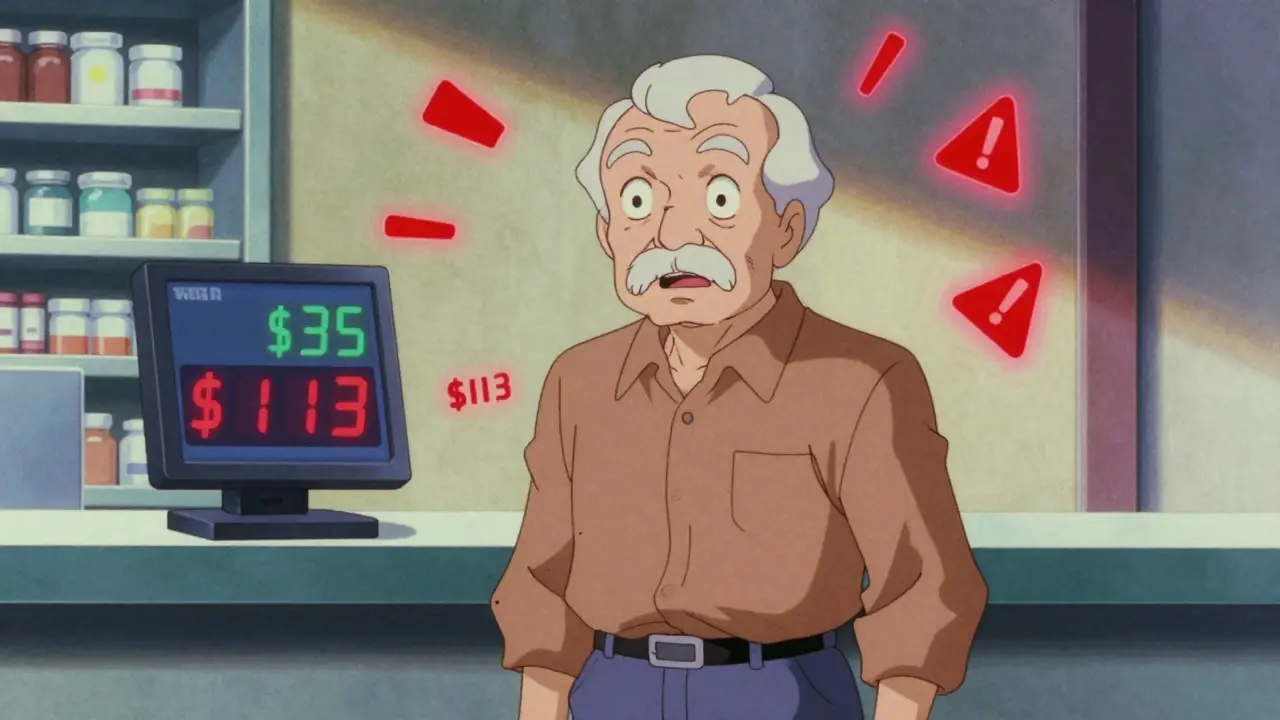

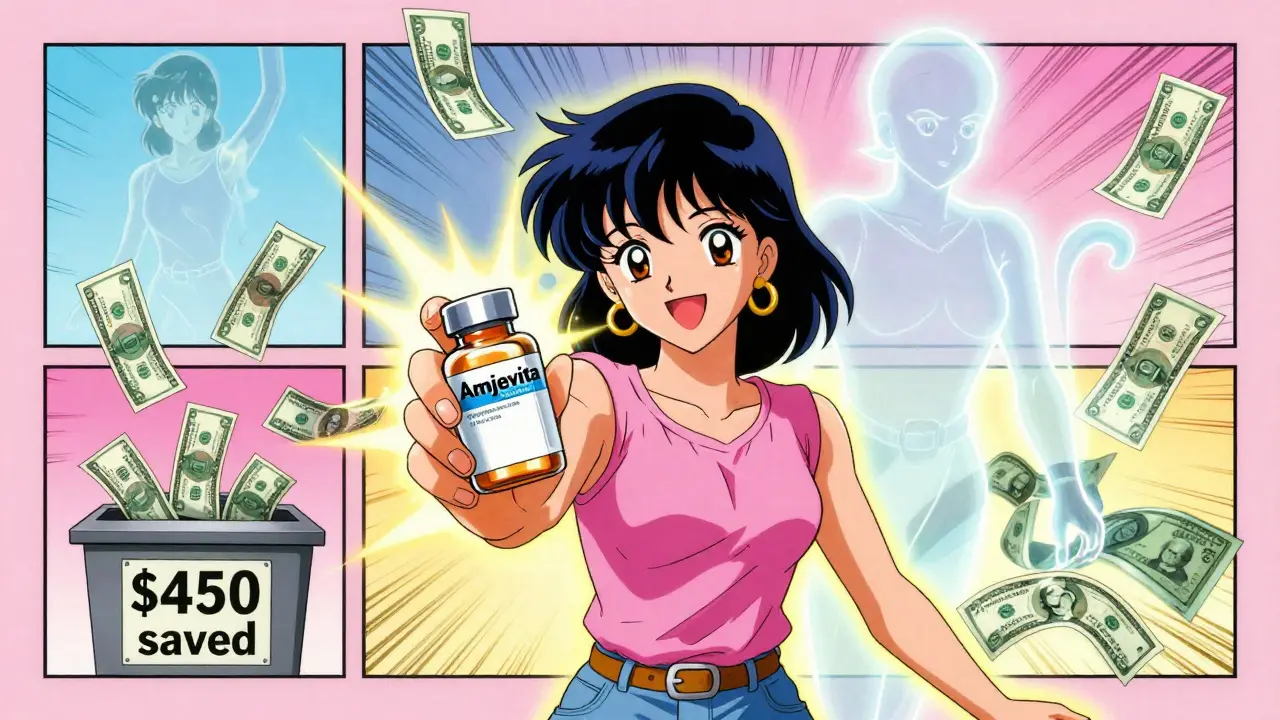

On January 1, 2025, millions of people on Medicare Part D woke up to find their prescription costs had changed-sometimes dramatically. A man in Ohio saw his insulin copay jump from $35 to $113 overnight. A woman in Florida switched from Humira to a biosimilar and saved $450 a month. These aren’t outliers. They’re the new reality of how insurance companies manage drug coverage. Formulary updates, the list of medications your plan will pay for, are changing faster and more aggressively than ever before. And if you’re taking any chronic medication, you need to know what’s happening and how to protect yourself.

What Exactly Is a Formulary?

A formulary is your insurance plan’s approved drug list. It’s not just a catalog-it’s a ranking system. Drugs are grouped into tiers, and each tier has a different price you pay. In 2025, most Medicare Part D plans use four tiers:- Tier 1: Preferred generics. These cost $1 to $10 per prescription. Think metformin for diabetes or lisinopril for blood pressure.

- Tier 2: Non-preferred generics and preferred brand-name drugs. Copays average $47.

- Tier 3: Non-preferred brand-name drugs. These can cost $113 or more.

- Tier 4 (Specialty): High-cost drugs like cancer treatments or biologics. You might pay $113 or 25% of the drug’s price, whichever is higher.

Insurers push you down the tiers-meaning they want you on the cheapest option possible. That’s where generic switching comes in. If your brand-name drug is on Tier 3, your plan may force you to switch to a generic version on Tier 1. Sometimes, they’ll even push you to a biosimilar-a cheaper version of a biologic drug like Humira or Enbrel.

Why Are Formularies Changing So Fast?

The big reason is the Inflation Reduction Act (IRA) of 2022. It didn’t just lower drug prices-it rewrote how insurance plans work. Starting in 2025, Medicare Part D eliminated the infamous "donut hole." That means once you hit $5,030 in drug spending, you get full coverage until you hit $8,000. After that, you pay only 5% of your drug costs.But here’s the catch: to make this work financially, insurers had to cut costs elsewhere. That’s where generics and biosimilars come in. PBMs (pharmacy benefit managers like CVS Caremark, OptumRx, and Express Scripts) now have a strong financial incentive to replace expensive brand-name drugs with cheaper alternatives. In 2025, 78% of standalone Part D plans made major moves toward generic substitution. That’s nearly 4 out of 5 plans.

And it’s not just generics. Biosimilars are exploding. In 2024 alone, the FDA approved 17 new biosimilars-a 34% jump from the year before. These aren’t knockoffs. They’re scientifically proven to work the same as the original biologic. Companies like Amjevita (for Humira) and Kanjinti (for Herceptin) are now replacing older versions on formularies. And insurers are pushing them hard.

What’s Being Removed? What’s Being Added?

In 2025, some drugs disappeared from formularies entirely. CVS Caremark removed nine specialty drugs, including Herzuma and Ogivri. UnitedHealthcare moved Humalog insulin to a higher tier. Cigna dropped several asthma medications from preferred status. These aren’t random. They’re targeted. If a cheaper alternative exists, the old drug gets pushed out.But it’s not all bad news. New drugs are being added too. CVS added 18 new medications to its 2025 formulary, including 11 specialty drugs-mostly biosimilars. Anthem and Aetna added more generic versions of diabetes and heart medications. The goal? Lower costs while keeping access to effective treatment.

Here’s what you need to watch for:

- Complete exclusions: Your drug is no longer covered at all.

- Tier reassignment: Your drug moved to a higher tier, so your copay jumped.

- Step therapy: You have to try a cheaper drug first before they’ll cover yours.

- Prior authorization: Your doctor has to prove you need the drug before the plan pays.

How to Find Out If Your Drug Is Affected

You won’t get a warning on TV or the news. Insurance companies are required to send you a notice-but only if they’re changing a drug you’re already taking. And they only have to send it 60 days before the change. For new generics, they only need 30 days’ notice.So don’t wait. Here’s what to do:

- Check your plan’s formulary online. Look for the "2025 Formulary" or "Drug List" section. It’s usually under "Member Resources."

- Search for every medication you take, including over-the-counter ones your doctor recommended.

- Compare your current copay to the 2025 estimate. If it’s higher, note it.

- Call your pharmacy. Pharmacists have access to real-time formulary data and can tell you if your drug is being changed.

- Ask your doctor to review your list. They can help you spot potential switches before January 1.

Many people miss this step. They assume their drug is safe because it’s been covered for years. That’s the trap. Formularies change every year. In 2024, 68% of Medicare beneficiaries reported worrying about changes to their medications. Don’t be one of them.

What If Your Drug Gets Removed?

If your drug is taken off the formulary, you have options. First, your plan must give you a 30-day transitional supply. That means you can still get your current medication for one month after the change.After that, you can file an exception request. There are two types:

- Standard exception: You ask for your drug to be covered anyway. Processing time: 72 hours. Approval rate: 82% for tier changes.

- Expedited exception: Use this if you’re at risk of serious harm without your drug (e.g., seizures, heart failure, uncontrolled diabetes). Processing time: 24 hours. Approval rate: Only 47% for completely excluded drugs.

Don’t assume your doctor’s note is enough. You need to fill out the form. Your doctor must explain why the generic or biosimilar won’t work for you. For example: "Patient has had two allergic reactions to generic versions of this drug." Or: "Patient has been stable on this brand for 5 years; switching caused loss of symptom control."

Some people give up after one denial. But you can appeal. If the first appeal fails, you can request a second review. Keep copies of every letter, email, and call log.

Should You Switch to a Biosimilar?

Biosimilars are the most misunderstood part of this whole system. Many people think they’re "inferior" or "cheap copies." They’re not. The FDA requires them to be "highly similar" to the original drug-with no clinically meaningful differences in safety or effectiveness.Real-world data backs this up. A 2024 study of 12,000 patients who switched from Humira to Amjevita showed no increase in flare-ups or side effects. Another study found 92% of patients on biosimilar infliximab reported the same results as before.

And the savings? Huge. One woman in Michigan switched from Enbrel to Eticovo and saved $5,800 a year. That’s nearly $500 a month.

But here’s the catch: not all biosimilars are created equal. Some are approved as "interchangeable," meaning the pharmacist can swap them without asking your doctor. Others aren’t. If your plan pushes you to a non-interchangeable biosimilar, your doctor must approve it. Don’t let the pharmacy make the switch without your consent.

What’s Coming in 2026?

The biggest change isn’t happening in 2025-it’s coming in 2026. The Medicare Drug Price Negotiation Program will require all Part D plans to cover 10 specific drugs that the government has negotiated prices for. These include:- Stelara (ustekinumab)

- Prolia (denosumab)

- Xolair (omalizumab)

That means even if your plan removed these drugs in 2025, they must bring them back in 2026. And you won’t pay more than $35 per month for them. This is a game-changer.

By 2029, that list will grow to 20 drugs. And the government will keep negotiating. That’s why PBMs are rushing to push biosimilars now-they know the high-cost originals are coming under price controls. The race is on to get patients off expensive drugs before the government steps in.

What You Can Do Right Now

You don’t have to wait for January 1 to act. Here’s your checklist:- Review your formulary before December 15. That’s when plans release their final lists.

- Call your pharmacist and ask: "Is my drug changing in 2025?" They’ll know before you do.

- Ask your doctor if there’s a generic or biosimilar option that’s been proven to work for you.

- Don’t panic if your drug is moved. File an exception. You have rights.

- Keep records of every change, every call, every denial. You might need them later.

And remember: you’re not alone. Over 53 million Americans are on Medicare Part D. Most of them are facing the same changes. The system is complex, but you’re not powerless. You have tools. You have rights. And you have time to prepare.

What Happens If You Do Nothing?

If you ignore formulary changes, you risk one of three things:- Your pharmacy refuses to fill your prescription because it’s no longer covered.

- You show up at the counter and are hit with a surprise bill-hundreds more than last year.

- You skip doses because you can’t afford it, and your condition gets worse.

None of those outcomes are inevitable. But they’re common. In 2024, 38% of people who requested exceptions waited 10 to 14 days for approval. That’s two weeks without medication. For someone with diabetes, heart disease, or rheumatoid arthritis, that’s dangerous.

Don’t gamble with your health. Take 30 minutes now to check your formulary. Call your pharmacy. Talk to your doctor. You’ll thank yourself in January.

How do I find my insurance plan’s 2025 formulary?

Log in to your plan’s website and look for "Drug List," "Formulary," or "2025 Coverage." Most plans post this by mid-November. If you can’t find it, call the member services number on your card and ask for the current year’s formulary document. Pharmacies can also pull it up for you using your prescription number.

Can my pharmacy switch my drug without telling me?

Only if your drug is labeled as "interchangeable" by the FDA and your plan allows it. For non-interchangeable biosimilars or generics, the pharmacist must contact your doctor for approval. Always ask: "Is this the same drug I was taking?" If the answer is vague, push for clarity. You have the right to know exactly what you’re getting.

Why do some people save money on biosimilars while others pay more?

It depends on your plan’s tier structure. If your brand-name drug was on Tier 3 and the biosimilar is on Tier 1, you’ll save. But if your plan moved the biosimilar to a higher tier (rare, but possible), you could pay more. Always compare the copay for your current drug to the new one before agreeing to a switch.

What if my doctor says I can’t switch?

Your doctor can file an exception request. They’ll need to write a letter explaining why the alternative won’t work for you-like past side effects, lack of effectiveness, or medical instability. Most plans approve these if the reasoning is solid. If denied, you can appeal. Keep copies of everything.

Are there any drugs that can’t be switched?

Yes. Medicare protects six classes of drugs from formulary restrictions: immunosuppressants, antidepressants, antipsychotics, anticonvulsants, antiretrovirals, and cancer drugs. These must be covered in full, and insurers can’t force switches. But outside those categories, almost any drug can be changed.

Peyton Feuer

January 6, 2026 AT 03:19Siobhan Goggin

January 7, 2026 AT 21:55Vikram Sujay

January 8, 2026 AT 12:52Jay Tejada

January 8, 2026 AT 16:34Shanna Sung

January 8, 2026 AT 20:04Allen Ye

January 9, 2026 AT 05:06mark etang

January 10, 2026 AT 14:03Clint Moser

January 12, 2026 AT 12:13jigisha Patel

January 12, 2026 AT 17:17Jason Stafford

January 13, 2026 AT 22:26Mandy Kowitz

January 15, 2026 AT 05:14Justin Lowans

January 15, 2026 AT 08:04Uzoamaka Nwankpa

January 16, 2026 AT 22:33