Have you ever looked at your Medicare Part D bill and wondered why one pill costs $5 while another similar pill costs $45? The answer usually lies in how your plan handles generic drug coverage. If you are on a fixed income, understanding this system isn't just about saving money; it is about keeping your heart medication, blood pressure drugs, or cholesterol treatments affordable.

The rules changed significantly starting in 2025 with the Inflation Reduction Act, and those changes continue to shape your costs in 2026. You now have a hard cap on what you pay out of pocket, but getting there requires knowing how formularies work. Let’s break down exactly how these lists determine what you pay, where generics sit in the hierarchy, and how you can use this knowledge to lower your bills.

What Is a Formulary and Why Does It Matter?

A formulary is simply the list of prescription drugs that your specific Medicare Part D plan agrees to cover. Think of it as a menu. Not every restaurant serves the same food, and not every insurance plan covers the same pills. Under federal law, managed by the Centers for Medicare & Medicaid Services (CMS), every Part D plan must include a wide range of medications, but they have flexibility in which specific brands or generics they prefer.

Here is the catch: if your doctor prescribes a drug that isn’t on your plan’s formulary, you might have to pay the full price yourself. This happens more often than you might think. Data shows that nearly two-thirds of beneficiaries face formulary differences when comparing plans. That means the plan that looks cheapest on paper might actually cost you more if your specific generic isn’t listed or is placed in an expensive tier.

Generic drugs make up about 92% of all prescriptions filled under Part D. Because they are so common, how your plan treats them defines your monthly budget. Unlike brand-name drugs, which often require prior authorization or step therapy, generics are usually easier to access-but only if you know which ones your plan favors.

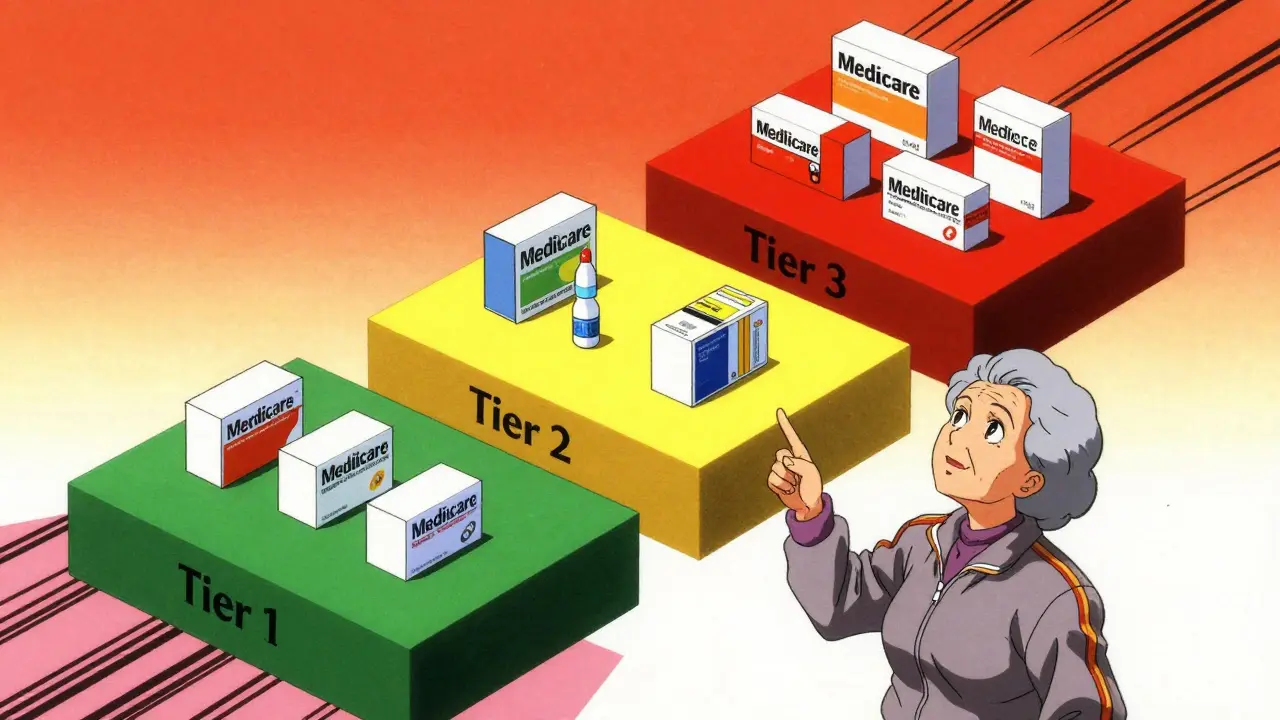

Understanding the Tier System

Your formulary is organized into tiers, like levels in a video game. Each level has a different cost attached to it. For generic drugs, you will mostly see two tiers:

- Tier 1: Preferred Generics: These are the lowest-cost options. Your copayment is often a flat fee, typically between $0 and $15 for a 30-day supply. Plans put their most cost-effective generics here to encourage you to choose them.

- Tier 2: Non-Preferred Generics: These are still generic versions of drugs, but your plan considers them slightly more expensive or less preferred. You might pay a higher flat copay (up to $40) or a percentage of the cost (coinsurance).

Brand-name drugs usually sit in Tiers 3, 4, or 5, where costs jump significantly. By steering you toward Tier 1 and 2 generics, plans save money-and if you follow suit, you do too. However, be careful. Just because a drug is generic doesn’t mean it is automatically Tier 1. Some newer generics might land in Tier 2 until the plan updates its preferences.

| Tier | Type | Typical Copay/Coin | Notes |

|---|---|---|---|

| Tier 1 | Preferred Generic | $0 - $15 | Lowest cost option |

| Tier 2 | Non-Preferred Generic | $15 - $40 or 25% | Slightly higher cost |

| Tier 3+ | Brand Name | $40 - $100+ | Often requires prior auth |

How Much Do You Pay in 2026?

The way you pay for these generics depends on which phase of coverage you are in during the year. The Inflation Reduction Act brought major relief, capping your total annual spending. Here is how the math works for 2026:

- Deductible Phase: Before any coverage kicks in, you pay 100% of the drug cost. In 2026, the standard deductible is likely around $615 (adjusted from 2025). Once you spend this amount, you move to the next phase.

- Initial Coverage Phase: After meeting the deductible, you typically pay 25% coinsurance for generic drugs. The plan pays the rest. This continues until your total out-of-pocket spending hits the cap.

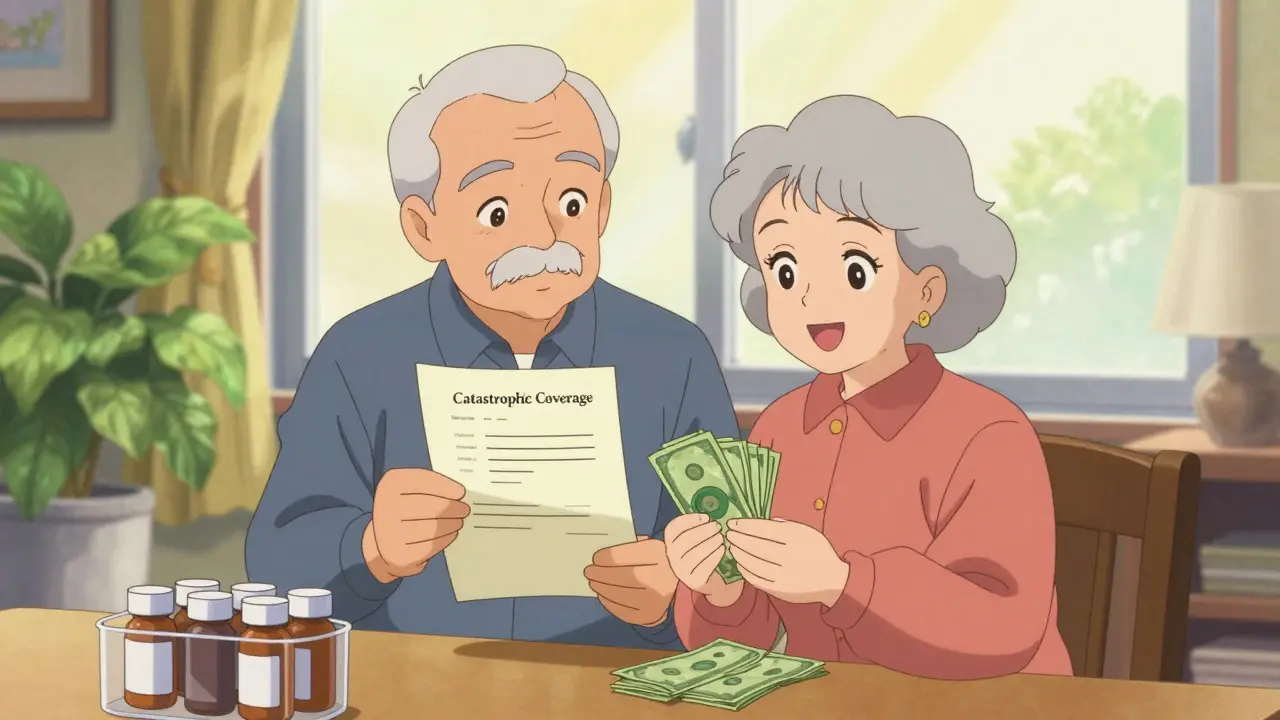

- Catastrophic Coverage: This is the big change. Once you hit the out-of-pocket cap-which is $2,100 in 2026-you pay $0 for the rest of the year. No more surprise bills. No more "donut hole" worries for generics.

It is crucial to understand what counts toward that $2,100 cap. For generic drugs, only the actual amount you pay (your copay or coinsurance) counts. This is different from brand-name drugs, where manufacturer discounts also count toward the threshold. So, if you take mostly generics, you need to track your real cash payments closely to know when you’ve hit the cap.

Common Pitfalls with Generic Substitution

You might assume that if a drug is generic, any pharmacy can dispense it. But Medicare Part D plans can be picky. A common issue arises with "therapeutic interchange." This happens when your plan covers Generic A but not Generic B, even though both treat the same condition.

If your pharmacist tries to substitute a generic that isn’t on your formulary, you could get stuck paying the full price. For example, if you need a blood pressure medication and your plan only covers Lisinopril (Tier 1) but not Enalapril (Tier 2 or excluded), asking for Enalapril without approval could lead to a hefty bill. Always check if your specific generic is on the formulary before picking it up.

Another trap is "authorized generics." These are brand-name drugs sold as generics by the same manufacturer. They look like generics and act like generics, but sometimes plans categorize them differently. While rare, this confusion can lead to unexpected costs. Always ask your pharmacist if the generic you are receiving is the exact match for your plan’s preferred list.

How to Optimize Your Generic Coverage

You don’t have to accept whatever your current plan offers. With some proactive steps, you can ensure you are getting the best deal on your generics.

- Review the ANOC Every Fall: Your Annual Notice of Change (ANOC) arrives in September. It lists any changes to your formulary for the coming year. Check if your generics have moved from Tier 1 to Tier 2. Even a small shift can add up over 12 months.

- Use the Plan Finder Tool: Don’t guess. Go to Medicare.gov and use the Plan Finder. Enter your specific medications. The tool will show you which plans cover your generics at the lowest tier. Research suggests beneficiaries who use this tool save an average of $427 annually.

- Request a Coverage Determination: If a needed generic is missing from your formulary, you can request an exception. Doctors can write letters explaining medical necessity. About 83% of these requests result in coverage approval, so it is worth the effort if your health depends on it.

- Consider Zero-Deductible Plans: If you take multiple generics, look for plans with a $0 deductible. About half of stand-alone Prescription Drug Plans (PDPs) offer this. It eliminates the initial hurdle of paying full price before coverage starts.

Looking Ahead: What Changes Are Coming?

The landscape for generic coverage continues to evolve. Starting in 2026, CMS requires plans to include a "generic price comparison tool" in their member portals. This will help you easily see if a cheaper therapeutic alternative exists for your condition. Additionally, the Medicare Drug Price Negotiation Program will begin affecting certain generics and biosimilars in later years, potentially driving prices down further.

Experts predict that by 2027, nearly all beneficiaries will have access to $0 copays for at least half of commonly prescribed generics. Until then, staying informed is your best defense against rising costs. Keep an eye on your statements, question high charges, and never hesitate to ask your pharmacist or plan representative for clarification.

What is the out-of-pocket cap for Medicare Part D in 2026?

The out-of-pocket cap for Medicare Part D in 2026 is $2,100. Once you have paid this amount in deductibles, copayments, and coinsurance for covered drugs, you enter catastrophic coverage and pay $0 for the remainder of the year.

Do all generic drugs cost the same in Medicare Part D?

No. Generic drugs are split into tiers. Tier 1 preferred generics usually have low fixed copays ($0-$15), while Tier 2 non-preferred generics may have higher copays or require coinsurance. The cost depends on your specific plan's formulary.

What happens if my generic drug is not on my plan's formulary?

If your drug is not on the formulary, you may have to pay the full price. However, you can request a "coverage determination" or exception through your plan. Your doctor can provide medical justification, and many such requests are approved.

How does the deductible affect generic drug coverage?

Before you meet your annual deductible (approximately $615 in 2026), you pay 100% of the drug cost. After meeting the deductible, you typically pay a smaller copay or 25% coinsurance for generics until you hit the out-of-pocket cap.

Can I switch plans if my generic moves to a higher tier?

Yes. During the Annual Enrollment Period (October 15 - December 7), you can switch to a different Part D plan that keeps your generic in a lower tier. Use the Medicare Plan Finder to compare costs before switching.

Mark Hogan

June 2, 2026 AT 23:40hey guys, just wanted to say that this info is super helpful for anyone trying to figure out their meds. i always get confused by the tiers but this breaks it down nicely. thanks for posting.

Dave Villeneue

June 4, 2026 AT 20:00The article fails to address the systemic inefficiencies inherent in private insurance models. The tier system is a mechanism of profit maximization disguised as cost control. Beneficiaries are forced into a labyrinth of bureaucratic hurdles where prior authorization serves only to delay treatment and increase administrative overhead. The so-called 'cap' is irrelevant if the initial deductible renders the coverage inaccessible to low-income individuals during critical periods of illness. This is not healthcare; it is managed decline.

Rachel Harrypersad

June 5, 2026 AT 08:03its funny how we pretend these changes matter when the whole system is broken anyway you pay more to get less care and then they tell you its your fault for not reading the fine print i feel like im screaming into a void sometimes because nobody really cares about the people who actually need help

Alexandre Desbiens

June 6, 2026 AT 16:38It is important to note that while the Inflation Reduction Act has introduced significant caps, the variability between plans remains a critical factor. Many beneficiaries overlook the distinction between preferred and non-preferred generics, leading to unexpected costs. One should meticulously review the Annual Notice of Change each September to ensure their medications remain in the lowest possible tier. The Medicare Plan Finder tool is an underutilized resource that can identify substantial savings opportunities across different Part D options.

Brian Irwin

June 8, 2026 AT 15:07i totally agree with alexandre here. its easy to forget to check those notices until its too late. my mom almost got stuck paying full price for her blood pressure med last year because she didnt realize it moved to tier 2. just a small reminder to everyone to look at their mail in september.

Wendy Engelmann

June 9, 2026 AT 15:20There is a certain irony in expecting elderly individuals to navigate complex pharmaceutical formularies without assistance. The cognitive load required to understand tier shifts, deductibles, and catastrophic coverage thresholds is immense. While tools exist, the accessibility of these resources varies widely. We must consider whether the current design of Medicare Part D truly supports the demographic it serves or merely shifts the burden of administration onto vulnerable populations.

Nicholas Bowling

June 11, 2026 AT 06:00everyone complains about the cost but no one wants to pay higher taxes to fix it. its all about entitlements and expecting free stuff. if you cant afford your meds maybe you should have saved money instead of spending it on vacations. stop blaming the system and take responsibility for your own choices

Lisa Thomas

June 11, 2026 AT 19:11oh wow that was harsh nick :/ i think most people here are just trying to survive on fixed incomes and every dollar counts. its not about being lazy its about the system being really confusing and expensive. we could all use a little more kindness here.

William Storm

June 12, 2026 AT 21:39One might argue that the complexity of the formulary system is intentional; it serves to obscure the true cost of care from the average consumer. The proliferation of tiers, copays, and coinsurance creates a fog of confusion that benefits the insurer. Furthermore, the reliance on self-management via online tools assumes a level of digital literacy and health literacy that is not universally present. This is a failure of design, not just policy.

Aswin Ashokan

June 13, 2026 AT 06:42medicare part d is a joke compared to what we have in india where generic drugs are affordable for everyone. why do americans accept such high prices and complicated rules? it shows a lack of discipline and poor understanding of basic economics. the system is designed to exploit ignorance and it works because people are too lazy to fight back

Francis Saul

June 14, 2026 AT 04:24look i know its frustrating but fighting each other doesnt help. we all just want to stay healthy and not go broke. if you are struggling please talk to your pharmacist they can often help find alternatives or apply for patient assistance programs. there is help out there you just gotta ask for it.

Alyssa Zucker

June 14, 2026 AT 05:51I read through this and it made me feel a bit anxious about my own plan. I didn't realize that even generics could be in different tiers. It's scary to think I might be overpaying without knowing it. I'm going to call my plan tomorrow to check where my current medications fall. Thank you for sharing this information, it really helps to have it laid out clearly.

Hassan Bukhari

June 15, 2026 AT 15:14the real issue is that most people here dont even understand what a formulary is. they blindly trust their doctors and pharmacists without doing any research. if you took five minutes to read the actual cms guidelines you would see that the system is actually quite logical once you grasp the basics. its pathetic how dependent people are on others to manage their basic health needs.